The Hidden Revenue Gaps in Companies Owned by Private Equity

Private equity ownership can create urgency, discipline, and capital for growth. It can also reveal a harder truth: many companies owned by private equity do not have a revenue problem that is visible in the headline numbers. They have a revenue system problem hiding beneath them.

The P&L may show growth. The board deck may show a healthy pipeline. The management team may be confident that demand exists. Yet when the sponsor pushes for faster expansion, improved EBITDA, or a buyer-ready exit story, revenue gaps start to appear.

These gaps are rarely dramatic at first. They show up as missed quarters, inconsistent rep performance, discounting pressure, slow enterprise deals, unexplained churn, or expansion plans that require more management effort than expected. Left unresolved, they reduce the quality of growth and make the investment thesis harder to defend.

For PE firms, operating partners, and portfolio company leaders, the question is not simply, “Can this company grow?” It is, “Can this company grow predictably, profitably, and without heroics?”

What Makes a Revenue Gap “Hidden”?

A hidden revenue gap is the difference between the revenue a company appears capable of producing and the revenue it can reliably produce through a repeatable commercial engine.

That distinction matters. A business can have strong historical sales and still lack a scalable go-to-market model. Founder relationships, a few exceptional salespeople, favorable market timing, or a concentrated customer base can all make revenue look stronger than it really is.

Hidden gaps usually have three characteristics.

They are camouflaged by growth. When revenue is rising, few people want to question whether it is repeatable. Growth can hide weak qualification, poor handoffs, low pricing discipline, and a lack of account expansion process.

They are spread across functions. Sales blames marketing for weak leads. Marketing blames sales for poor follow-up. Finance sees margin leakage but not the commercial behavior causing it. Operations sees delivery strain but not the customer promise that created it.

They are rationalized as normal business noise. A missed quarter becomes “seasonality.” A weak forecast becomes “deal timing.” A stalled new market becomes “longer ramp.” Sometimes those explanations are true. Often, they are symptoms of a revenue engine that was never fully built.

Why Companies Owned by Private Equity Are Especially Exposed

PE-backed companies operate under a different commercial clock. The sponsor is not evaluating growth in isolation. It is evaluating growth against hold period constraints, debt service, value creation plans, management capacity, and exit expectations.

That pressure changes the meaning of revenue performance. A founder-owned business can tolerate inconsistent sales motion if relationships keep the business moving. A strategic acquirer may absorb inefficiencies into a larger platform. A PE-owned company has less room for ambiguity because the investment case depends on proving that growth is not accidental.

The transition after acquisition often exposes these issues. Reporting becomes more rigorous. Targets become more specific. Management teams are asked to segment customers, defend pricing, expand accounts, enter new markets, or professionalize sales management. If the commercial infrastructure is thin, the gap between the thesis and execution widens quickly.

This is one reason many sponsors find that the problem is not the original investment logic, but the operating system needed to deliver it. For a deeper look at execution risk after close, see this discussion of why PE firms miss growth targets after acquisition.

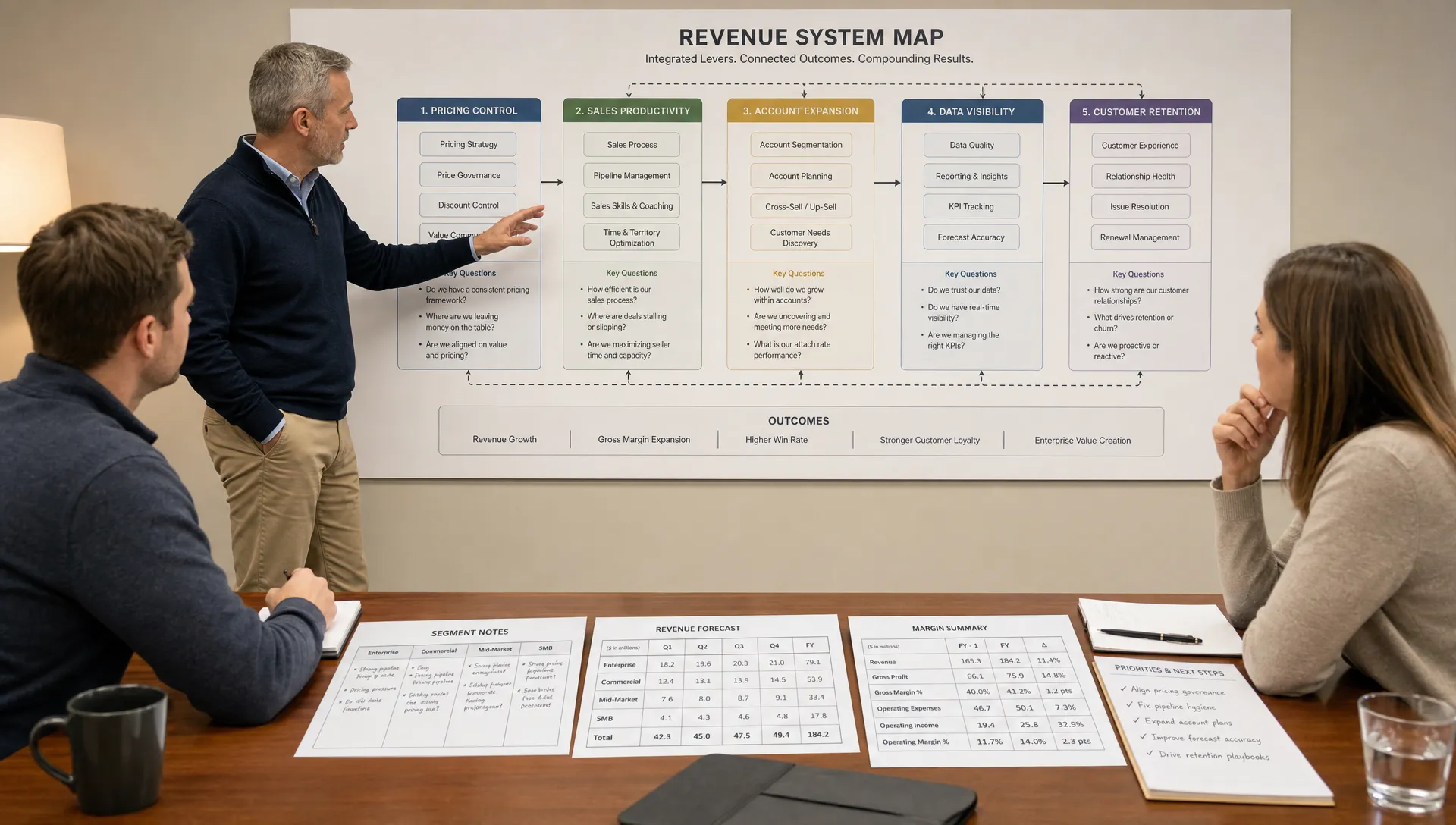

The Most Common Hidden Revenue Gaps

Revenue gaps vary by sector, business model, and maturity stage, but the patterns are consistent. The most valuable diagnostic work often starts by separating top-line growth from the operating behaviors that produce it.

| Hidden revenue gap | How it hides | Why it matters to PE owners |

|---|---|---|

| ICP drift | Sales accepts revenue from customers outside the best-fit profile | Growth becomes harder to repeat and more expensive to service |

| Forecast inflation | Pipeline appears large but lacks stage discipline | Board visibility declines and resource planning becomes unreliable |

| Pricing leakage | Discounts, concessions, and scope creep are treated as deal-level exceptions | EBITDA improvement is delayed even when revenue grows |

| Account expansion weakness | Customer success or account management lacks a structured upsell motion | The company overdepends on new logos to hit targets |

| Sales productivity variance | A small number of reps or leaders carry the number | Scaling headcount does not translate into scaling revenue |

| Channel dependency | Growth relies heavily on one partner, marketplace, or referral source | The revenue base becomes vulnerable to external decisions |

| Poor lead-to-close conversion | Marketing activity is measured, but commercial conversion is not | Spend increases without a clear link to bookings |

| CRM and finance mismatch | Sales, revenue operations, and finance work from different data | Management cannot see the true revenue picture quickly enough |

| Margin-blind growth | Teams pursue revenue without visibility into delivery cost or customer profitability | Growth reduces exit quality instead of improving it |

The danger is not that one of these gaps exists. Most portfolio companies have several. The danger is treating them as isolated functional issues rather than symptoms of a commercial system that needs to be installed or upgraded.

Revenue Quality Is Not the Same as Revenue Volume

One of the biggest mistakes in PE value creation is assuming that more revenue automatically means more enterprise value. Buyers rarely reward revenue equally. They reward revenue that is predictable, profitable, diversified, and defensible.

A company may grow 20 percent year over year, but if that growth comes from low-margin customers, heavy discounting, custom delivery, or a handful of relationships controlled by the founder, the quality of that revenue is weaker than the headline suggests.

This is especially important as the company approaches an exit. A buyer will ask whether revenue can continue without the current owner, sponsor intensity, or unusual market tailwinds. They will examine customer concentration, cohort performance, backlog quality, sales productivity, pipeline hygiene, churn drivers, and gross margin by segment.

That means PE owners should not wait until exit preparation to clean up the revenue story. The best exit evidence is built during the hold period. If the goal is to command a stronger valuation, the company needs proof that the commercial engine works, not just a narrative that it should work. This is closely tied to the way private equity companies improve exit readiness by building buyer-ready evidence before the sale process begins.

The Founder-Led Revenue Trap

Many attractive acquisition targets grow because the founder or CEO is deeply involved in sales. That can be a strength before the deal. It becomes a risk after the deal if the revenue engine still depends on that person’s network, credibility, product knowledge, or deal control.

Founder-led selling often hides missing infrastructure. There may be no clear qualification process because the founder intuitively knows which deals matter. There may be no formal account expansion playbook because the founder personally spots opportunities. There may be no pricing discipline because exceptions are negotiated informally.

Once PE ownership pushes for scale, these informal systems break. New sales hires cannot replicate the founder’s pattern recognition. Marketing cannot target the right prospects because the ICP exists in someone’s head. Customer success cannot expand accounts because the commercial promise was never translated into a repeatable process.

The solution is not to remove the founder from revenue overnight. In many cases, their market insight is invaluable. The solution is to extract that insight, codify it, and turn it into a commercial operating system that others can run.

The Data Gap: When CRM, ERP, and Finance Do Not Agree

Revenue gaps are harder to close when the company cannot trust its own data. This is common in mid-market portfolio companies that have grown through founder-led processes, acquisitions, or partial system implementations.

The CRM may show a strong pipeline, while finance sees delayed invoicing or weak collections. The ERP may contain the reality of bookings, delivery, and billing, while sales leaders rely on spreadsheets. Customer profitability may be impossible to analyze without manual reconciliation. The leadership team ends up debating whose number is correct instead of deciding what to do next.

For companies using NetSuite or similar platforms, revenue visibility depends on clean workflows, reliable integrations, and rapid diagnosis when something breaks. This is where specialist partners such as AI and NetSuite consulting for mid-market companies can be relevant, particularly when technical debt, configuration drift, or fragmented system notes are slowing down operational decision-making.

The commercial lesson is simple: if the revenue system cannot produce a trusted view of pipeline, bookings, margin, retention, and cash conversion, management is steering with partial information.

Pricing Leakage Is Often Bigger Than the Team Thinks

Pricing is one of the fastest ways to improve value, but it is also one of the most politically sensitive. Sales teams worry about losing deals. Account managers worry about damaging relationships. Operators worry about customer escalations. As a result, pricing leakage often hides inside normal commercial behavior.

It may appear as excessive discounting to close quarter-end deals. It may show up as custom scope that is not reflected in the contract. It may come through weak renewal increases, inconsistent payment terms, or legacy customers that have never been repriced.

The issue is not always that prices are too low. Sometimes the real gap is that pricing authority is unclear. Reps do not know when to hold the line. Managers approve exceptions without tracking patterns. Finance sees the margin impact after the deal is already signed.

PE owners should treat pricing as a governance issue, not just a sales tactic. The company needs clear discount thresholds, escalation rules, margin visibility, customer segmentation, and a cadence for reviewing exceptions. Even modest improvements can create meaningful EBITDA impact when applied across the revenue base.

Sales Productivity Variance Can Break the Growth Plan

Another hidden gap is the difference between average sales productivity and scalable sales productivity. A company may hit its number because two senior reps outperform, while newer hires take too long to ramp or never reach quota. On the surface, the sales team looks effective. Underneath, the hiring model is not working.

This matters because many PE growth plans assume that adding sales capacity will increase bookings. That assumption only holds if the company has a defined ICP, repeatable messaging, clear sales stages, effective onboarding, and managers who can coach performance.

If these elements are missing, new headcount can increase cost faster than revenue. The board sees the investment in growth, but the bookings lag. Sales leadership asks for more time. Finance questions the plan. The sponsor loses confidence in the forecast.

A practical diagnostic is to compare rep performance by cohort. Look at ramp time, pipeline creation, conversion rate, average deal size, discounting, win rate, and retention quality of customers sold. If performance depends heavily on tenure or individual heroics, the sales model is not yet institutional.

Account Expansion Is the Underused Lever

Many portfolio companies overinvest in new logo acquisition while underbuilding account expansion. This is a costly mistake, especially in B2B businesses with long sales cycles or high customer acquisition costs.

The expansion gap often exists because ownership of the customer is unclear after the initial sale. Sales moves on to new prospects. Customer success focuses on retention or service delivery. Account management is reactive. No one owns a structured process for identifying cross-sell, upsell, renewal improvement, or executive relationship expansion.

For PE-backed companies, this is a missed opportunity. Existing customers can provide faster, more profitable growth if the company understands usage, satisfaction, unmet needs, and buying centers. Expansion also strengthens exit readiness because it demonstrates that the company can grow customer value over time.

The fix is not simply to tell account managers to sell more. The company needs segmentation, account plans, expansion triggers, customer health indicators, executive sponsorship, and commercial offers that make sense for existing buyers.

How to Diagnose Hidden Revenue Gaps

A useful revenue diagnostic does not start with opinions. It starts with evidence. The goal is to identify which gaps are constraining value creation and which can be fixed within the hold period.

Start with revenue segmentation. Break revenue down by customer type, product, geography, channel, margin, tenure, and acquisition source. This often reveals that the most attractive revenue is coming from a narrower segment than the company has been pursuing.

Then map the funnel from demand creation to cash collection. Look at lead source, qualification, stage conversion, sales cycle length, proposal-to-close rate, discounting, implementation timing, invoicing, and collections. This shows where commercial momentum is being lost.

Next, examine customer economics. Compare acquisition cost, gross margin, retention, expansion, service intensity, and support burden by segment. A customer group that looks attractive on revenue may be unattractive once delivery cost and churn risk are included.

Finally, test management cadence. Ask whether the leadership team reviews the same commercial facts every week. If the company lacks a common operating rhythm, even good analysis will not translate into execution.

Which Gaps Should PE Owners Fix First?

Not every issue deserves immediate attention. The right priority depends on the investment thesis, exit timeline, and the scale of value at stake. A company preparing for sale needs evidence and risk reduction. A platform company early in the hold period may need infrastructure before aggressive growth. A business pursuing add-ons may need integration discipline and unified reporting.

A practical way to prioritize is to score each revenue gap by value potential, urgency, execution difficulty, and dependency risk.

| Priority question | What it reveals |

|---|---|

| Will fixing this improve EBITDA, growth rate, or revenue quality within the hold period? | Value creation relevance |

| Does this gap weaken the exit story if left unresolved? | Buyer perception risk |

| Can management execute the fix with current capacity? | Operational feasibility |

| Does another initiative depend on this being fixed first? | Sequencing risk |

| Can progress be measured in 30 to 90 days? | Accountability and momentum |

This prevents teams from chasing interesting problems instead of valuable ones. For example, a full CRM rebuild may be useful, but if pricing leakage is costing margin every quarter, pricing governance may deserve priority. Similarly, market expansion may be attractive, but if the core sales process is inconsistent, expansion can magnify the weakness.

A 90-Day Approach to Closing the Most Valuable Gaps

The first 90 days of a revenue improvement effort should create clarity, momentum, and measurable behavioral change. It should not become an endless strategy exercise.

In the first 30 days, establish the facts. Reconcile the commercial data, segment revenue, interview customer-facing teams, review lost deals, inspect pipeline quality, and identify where the investment thesis depends on assumptions that have not been operationalized.

In days 31 to 60, select a small number of high-value fixes. These may include tightening ICP definitions, changing qualification rules, introducing pricing approval thresholds, rebuilding pipeline stages, creating account expansion plays, or installing a weekly revenue cadence.

In days 61 to 90, turn the fixes into management routines. Assign owners, define metrics, review progress weekly, and remove friction quickly. The objective is not perfection. It is to prove that the company can identify a revenue constraint, act on it, and produce measurable improvement.

This is where PE discipline can be a real advantage. Sponsors can help management focus, sequence initiatives, and avoid spreading effort across too many priorities at once.

Warning Signs That Revenue Gaps Are Already Costing Value

Hidden gaps become visible if you know what to look for. Sponsors and leadership teams should pay attention when the same issues appear repeatedly under different labels.

- Pipeline coverage looks healthy, but forecast accuracy remains poor.

- New sales hires are added, but bookings do not scale proportionally.

- Revenue grows while gross margin, cash conversion, or delivery quality weakens.

- The CEO or founder is still required to close too many important deals.

- Lost deal reasons are vague, inconsistent, or not captured at all.

- The company cannot quickly explain revenue by segment, margin, channel, and retention.

- Account expansion depends on customer requests rather than proactive plays.

- Sales and finance disagree on bookings, revenue timing, or customer profitability.

When these signals appear, pushing harder on growth can make the problem worse. Before adding headcount, entering a new market, or increasing marketing spend, PE owners should ensure the commercial foundation can support the next stage. That principle is central to deciding what PE funds should fix before pushing growth.

Frequently Asked Questions

What are revenue gaps in companies owned by private equity? Revenue gaps are weaknesses that prevent a company from turning market opportunity into predictable, profitable growth. They may involve pricing, forecasting, sales productivity, customer expansion, data visibility, or revenue quality.

Why do these gaps often appear after acquisition? PE ownership introduces tighter targets, more rigorous reporting, and a defined hold period. Commercial weaknesses that were manageable in a founder-led environment become more visible when the company is asked to scale faster and prove repeatability.

Are hidden revenue gaps mainly a sales problem? Not usually. Sales may be where the symptoms appear, but the cause often spans marketing, finance, operations, customer success, systems, and leadership cadence. The fix is a commercial operating system, not just more sales activity.

Should PE firms diagnose revenue gaps before or after closing? Ideally, both. Pre-close diligence can identify major commercial risks, but post-close diagnostics reveal how the company actually operates under PE ownership. The earlier the sponsor identifies the gaps, the more time there is to convert fixes into value.

How quickly can a portfolio company close revenue gaps? Some gaps, such as pricing governance or forecast discipline, can improve within a quarter. Others, such as sales productivity, account expansion, or system integration, may take several quarters. The key is to prioritize fixes that create measurable value within the hold period.

Turn Hidden Revenue Gaps Into Value Creation

The most valuable companies owned by private equity do not just grow. They prove that growth is repeatable, measurable, and resilient.

If your portfolio company is missing targets, relying on founder-led sales, struggling with forecast accuracy, or preparing for exit, the issue may not be demand. It may be hidden revenue gaps inside the commercial system.

Phil Pelucha Consulting helps PE firms, investors, and portfolio companies diagnose revenue constraints, install stronger commercial infrastructure, and accelerate value creation. To explore how an independent commercial diagnostic or revenue acceleration engagement could support your portfolio, visit Phil Pelucha Consulting.