What a Venture Partner Really Does in Portfolio Growth

Most portfolio companies do not fail to grow because no one had ideas. They fail because the right ideas never become a focused operating rhythm.

That is where a venture partner can become highly valuable. Not as a famous name on a fund website. Not as a casual connector who makes a few introductions. A strong venture partner helps turn investor ambition into portfolio growth by sharpening the commercial strategy, removing execution friction, and giving founders or management teams access to pattern recognition they do not yet have internally.

For PE, VC, family offices, and portfolio executives, the real question is not what the title sounds like. It is whether the venture partner helps the company grow faster, with less waste, and with better evidence for the next financing event, strategic partnership, or exit.

The venture partner role is often misunderstood

The title venture partner is used differently across funds. In some firms, a venture partner helps source deals and evaluate markets. In others, they are an experienced operator who works with selected portfolio companies after investment. Some are part-time. Some are deeply embedded. Some focus on one sector, such as fintech, SaaS, health, industrials, or consumer brands.

In portfolio growth, the role should be more precise. A venture partner is a senior commercial or sector expert who helps a company make better growth decisions and execute them faster. Their value comes from judgment, access, operating experience, and the ability to translate a fund’s investment thesis into practical action.

The best ones sit between the board and the operating team. They are close enough to understand the messy details of execution, but senior enough to see patterns across companies, markets, and capital cycles.

The worst version of the role is ceremonial. The venture partner appears in pitch decks, joins occasional calls, and introduces the company to a few contacts. That can be useful, but it rarely changes growth trajectory. Real portfolio growth requires more structure.

The real mandate: turn the investment thesis into commercial execution

When a company takes institutional capital, the growth clock changes. The business is no longer optimizing only for survival or steady organic progress. It now has to prove a specific thesis within a defined time horizon. That may mean faster revenue growth, stronger unit economics, expansion into a new market, better enterprise readiness, or evidence that the company can scale repeatably.

This is why venture capital changes GTM strategy so dramatically. Capital does not simply provide more budget. It changes the level of proof expected from the commercial engine.

A venture partner helps answer the questions that sit between ambition and execution:

- Which customer segment deserves priority now?

- Which sales motion can scale without destroying margin?

- Which partnerships can accelerate trust, distribution, or category adoption?

- Which commercial risks will matter most to future investors or acquirers?

- Which growth activities are distractions, even if they look exciting?

That last question is often the most valuable. Growth is not just about adding more campaigns, hires, markets, or channels. It is about choosing the few moves that compound.

What a venture partner actually does for portfolio growth

A venture partner’s contribution should be practical. The output is not advice for its own sake. It is better prioritization, faster learning, cleaner accountability, and stronger commercial evidence.

Diagnoses the real growth bottleneck

Before recommending a new hire, channel, partnership, or market, a strong venture partner identifies the constraint. Many portfolio companies misdiagnose their growth problem. They think they need more leads when the issue is poor ICP discipline. They think they need a larger sales team when the issue is weak conversion. They think they need US expansion when the current market motion has not yet become repeatable.

This is where external pattern recognition matters. A venture partner who has seen similar companies scale can separate symptoms from root causes. The diagnosis may reveal that the company needs sharper positioning, better sales process, improved customer success, stronger pricing discipline, or clearer segmentation before adding more growth spend.

That aligns closely with the principle that funds should understand what the portfolio company needs before scaling, rather than assuming growth headcount alone will solve the problem.

Sharpens the go-to-market focus

Founders and management teams often have too many growth options. A venture partner helps narrow the field. They can test whether the company is targeting the right buyer, whether the sales motion fits the average contract value, whether the message matches market urgency, and whether the pipeline reflects the ideal customer profile.

This is especially important when a company is moving from founder-led selling to a scalable commercial function. The venture partner helps convert intuition into repeatable process. That might include clarifying the ICP, refining qualification criteria, improving sales stage definitions, strengthening partner strategy, or aligning marketing with the actual revenue motion.

Creates market access that converts

Introductions are only valuable when they are strategic. A weak venture partner sends a list of names. A strong venture partner explains why each relationship matters, how to approach it, what commercial hypothesis it tests, and what follow-up should look like.

In some sectors, market access is not just about meeting buyers. It is about understanding the trust mechanisms that drive adoption. Consider categories where reimbursement, personalization, and expert guidance shape customer decisions. A venture partner evaluating a health and wellness model might study how personal training and nutrition coaching covered by insurance is positioned, because the growth question is not only demand generation. It is also buyer trust, eligibility, conversion friction, and long-term engagement.

That is the difference between networking and portfolio growth. The venture partner is not merely opening doors. They are helping the company learn faster from the right doors.

Builds a commercial operating cadence

Many portfolio companies have goals, but not a reliable cadence for achieving them. A venture partner can help create a rhythm around pipeline reviews, market feedback, strategic accounts, channel experiments, and leading indicators.

This does not mean micromanaging the CEO or CRO. It means helping leadership distinguish between activity and progress. The commercial cadence should make it obvious which assumptions are being tested, which metrics are improving, and which decisions need to be made.

| Portfolio growth moment | Venture partner contribution | Why it matters |

|---|---|---|

| First 90 days post-investment | Pressure-tests the growth thesis and identifies commercial gaps | Prevents the company from scaling a weak motion |

| Founder-led sales transition | Helps define ICP, sales process, and handoff points | Makes revenue less dependent on the founder |

| Market expansion | Assesses readiness, channel fit, and local buyer dynamics | Reduces wasted spend in new markets |

| Strategic partnerships | Prioritizes partners that improve distribution or credibility | Turns relationships into measurable growth |

| Next round or exit preparation | Builds evidence of repeatable growth and revenue quality | Improves investor or buyer confidence |

Venture partner vs operating partner vs advisor vs fractional CRO

The venture partner role often overlaps with other growth support roles, but it should not be confused with them. Clear role definition prevents frustration for both the fund and the portfolio company.

| Role | Typical position | Primary contribution | Common risk |

|---|---|---|---|

| Venture partner | Attached to a fund, often sector or growth focused | Pattern recognition, market access, GTM guidance, strategic support | Too informal if no mandate is defined |

| Operating partner | Usually fund-level, often more hands-on in PE | Operational improvement, management support, value creation plan execution | Can become too broad without clear priorities |

| Advisor | External expert or specialist | Targeted advice, credibility, or introductions | Limited accountability for implementation |

| Fractional CRO | Embedded commercial executive | Owns revenue leadership, sales process, and GTM execution | May be too tactical if strategy is unresolved |

In private equity, the closest comparison is often the operating partner. The difference is that an operating partner may have a broader mandate across the value creation plan, while a venture partner is often more focused on market insight, growth strategy, sector access, or founder support. For a deeper PE-focused comparison, the operating partner playbook for revenue growth shows how hands-on commercial value creation should be structured.

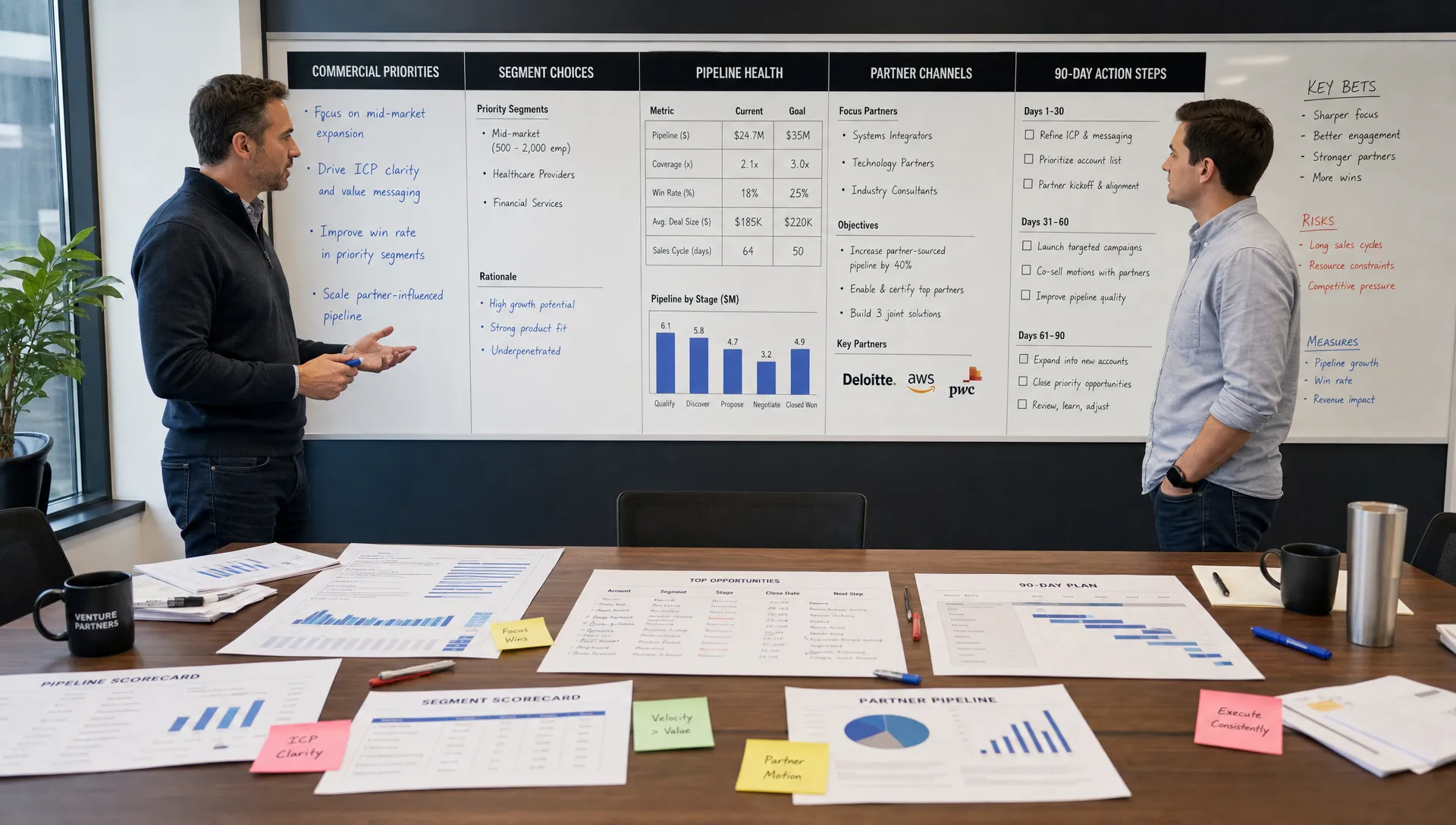

What good looks like in the first 90 days

A venture partner does not need to solve everything immediately. In fact, trying to fix too many issues at once is usually a sign of weak prioritization. The first 90 days should create clarity, focus, and momentum.

| Period | Focus | Practical output |

|---|---|---|

| Days 0 to 30 | Commercial diagnosis | Growth bottleneck, ICP assessment, sales motion review, priority risks |

| Days 31 to 60 | Strategy translation | Focused GTM priorities, partnership targets, operating cadence, decision rules |

| Days 61 to 90 | Execution support | Pilot initiatives, pipeline quality improvements, market feedback loops, leadership alignment |

The most important output is not a slide deck. It is a shared view of what must happen next and what the company will stop doing. A venture partner should create decision velocity.

That means the CEO, CRO, board, and sponsor understand the same growth priorities. It also means the company has a way to measure whether the advice is working.

Metrics a venture partner should influence

A venture partner may not own the revenue number directly, unless that is part of a formal operating role. But they should influence the quality of the commercial system that produces revenue.

Useful metrics include pipeline quality, stage conversion, sales cycle length, win rate by ICP segment, average contract value, net revenue retention, channel contribution, partner-sourced pipeline, gross margin by customer segment, and market expansion progress.

The right metrics depend on the company’s stage. An early-stage VC-backed company may need proof of repeatable demand and early sales efficiency. A PE-backed portfolio company may need stronger forecasting, management cadence, sales productivity, and exit-ready revenue evidence.

The venture partner’s job is to make the commercial story more credible. If revenue is growing but the source of growth is unclear, buyers and investors may discount it. If growth is concentrated in a few relationships, one channel, or founder-led selling, the company may look riskier than the headline numbers suggest.

Where funds get the role wrong

Funds often underuse venture partners because the role is poorly designed. The person may have strong experience, but no clear mandate. Or the company may not know whether the venture partner is an advisor, board observer, operator, or sponsor representative.

Common mistakes include:

- Choosing a venture partner for reputation rather than relevant operating pattern recognition.

- Asking for introductions before diagnosing the commercial constraint.

- Giving advice without defining who owns execution.

- Creating too many workstreams instead of focusing on the few that move enterprise value.

- Failing to measure whether the venture partner’s involvement improves growth quality.

The founder or management team also needs to trust the process. If the venture partner is perceived as a surveillance mechanism for the fund, the relationship becomes defensive. If they are positioned as a practical resource with a clear mandate, the team is far more likely to use them well.

How sponsors and founders should use a venture partner

A venture partner is most effective when the fund and company agree on five things: the objective, the decision rights, the operating cadence, the metrics, and the expected time commitment.

For example, a venture partner might be assigned to help a company validate enterprise demand in a new vertical, prepare the sales organization for a larger round, improve partner-led growth, or support the transition from founder-led sales to a managed revenue function.

The mandate should be specific enough to create accountability, but flexible enough to adapt as new evidence emerges. Portfolio growth is rarely linear. The value of a venture partner is that they help leadership interpret signals quickly and make better decisions under uncertainty.

The best venture partners do not replace management. They make management better.

Frequently Asked Questions

What does a venture partner do? A venture partner supports a fund and its portfolio companies through market insight, deal support, strategic guidance, introductions, and growth execution advice. In portfolio growth, their role is to help companies turn the investment thesis into measurable commercial progress.

Is a venture partner part of the management team? Usually, no. A venture partner typically sits outside the company’s formal management structure unless they are given a defined operating role. They advise, connect, challenge, and support execution, but accountability must be clearly assigned.

How is a venture partner different from an advisor? An advisor often provides narrow expertise or credibility. A venture partner is usually more connected to the fund’s portfolio strategy and may be involved across multiple companies, sectors, or investment stages.

When should a portfolio company use a venture partner? The role is most valuable during moments of growth complexity, such as post-investment planning, market expansion, GTM redesign, strategic partnership development, sales leadership transition, or preparation for a financing event or exit.

How should a fund measure venture partner impact? Measurement should focus on commercial progress, not activity. Useful indicators include better ICP clarity, improved pipeline quality, higher conversion, shorter sales cycles, stronger partner contribution, clearer management cadence, and better evidence for future investors or acquirers.

Turn venture partner insight into portfolio growth infrastructure

A venture partner can create enormous value, but only when their insight becomes part of a repeatable commercial operating system. Portfolio growth requires diagnosis, prioritization, execution cadence, and evidence that revenue can scale.

Phil Pelucha Consulting works with PE firms, VC investors, family offices, and portfolio companies on revenue acceleration, commercial diagnostics, fractional CRO support, GTM optimization, market expansion, and AI-powered automation. If your portfolio needs more than advice, the next step is to turn growth intent into infrastructure that compounds.