What Growth Equity Firms Want Before They Invest

Growth equity firms do not invest because a company is growing. They invest because the growth appears repeatable, capital efficient, and large enough to justify institutional risk.

That distinction matters. A founder may see a rising revenue line and assume the company is ready for growth capital. An investor sees a set of questions: Why is revenue growing? Which customers are driving it? Can the team repeat the motion without heroic effort? Will additional capital accelerate value creation, or will it expose weaknesses in sales, data, hiring, and execution?

Before they invest, growth equity firms want evidence that capital can scale a commercial system that already works. They are not looking for a perfect company. They are looking for a company where the risks are understood, the upside is specific, and the next stage of growth can be managed with discipline.

The growth equity mindset: proof before potential

Growth equity sits between early-stage venture capital and traditional buyout investing. The company is usually beyond the idea stage. It has customers, revenue traction, a product or service that the market has validated, and a management team that has already built meaningful momentum.

But unlike a buyout investor, a growth equity investor may not be underwriting a full operational reset. The investment thesis often depends on accelerating what is already working. That could mean expanding into a new market, professionalizing sales, investing in customer success, building a partner channel, improving revenue operations, or supporting strategic hiring.

The core question is simple: If we add capital, expertise, and time, does this company become materially more valuable without relying on luck?

That is why the best growth equity conversations are less about the pitch deck and more about the operating evidence underneath it.

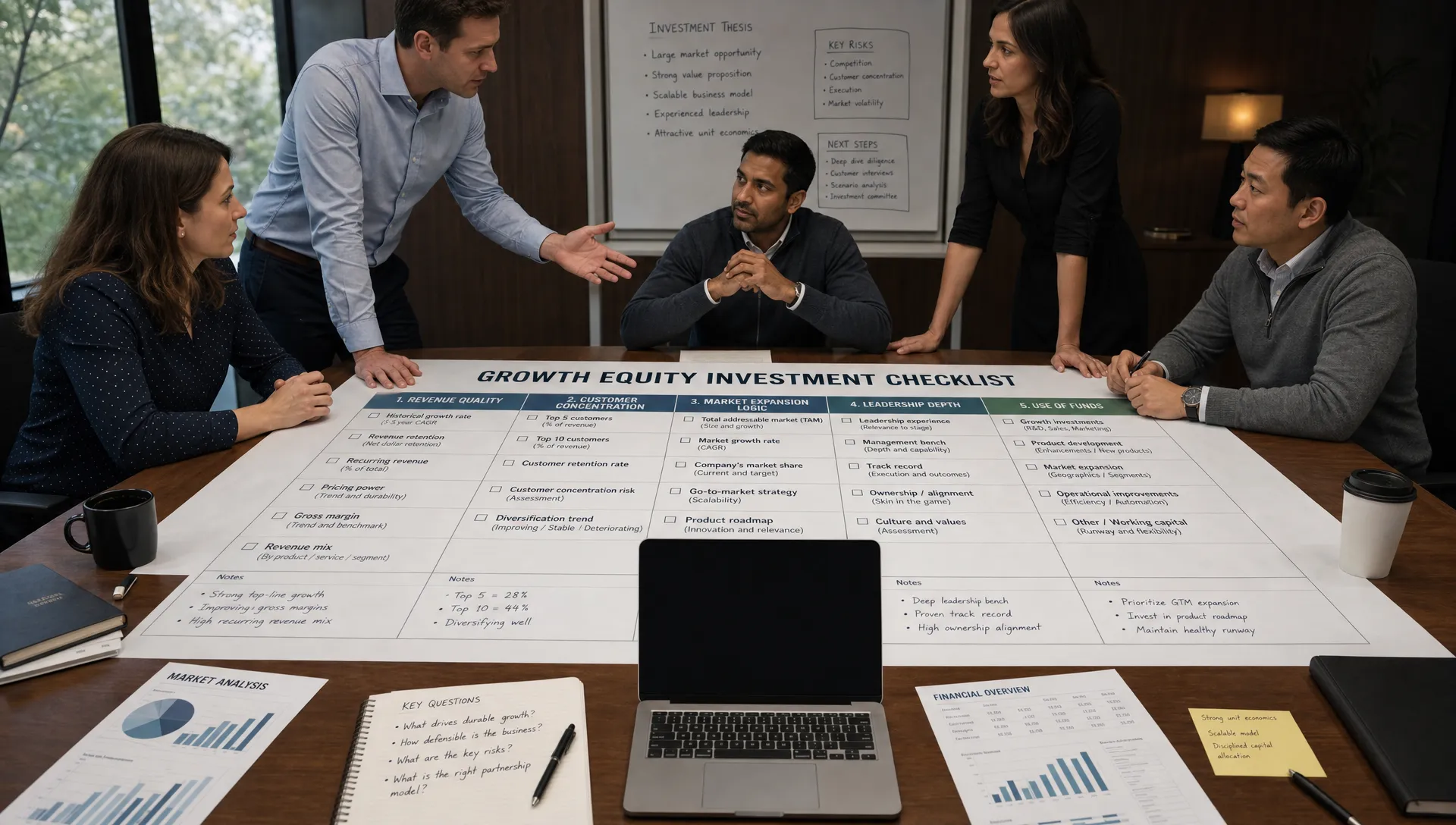

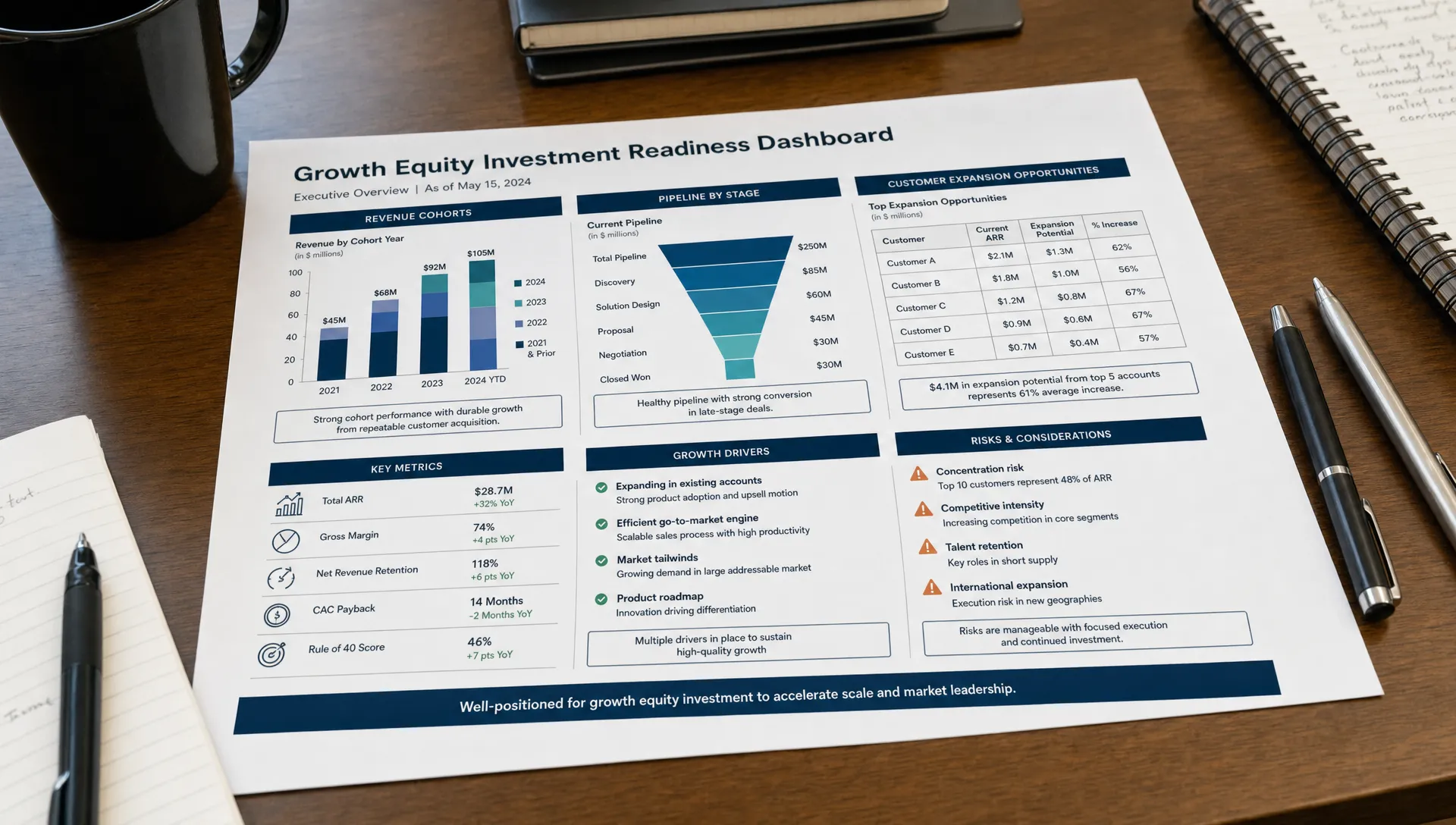

1. Revenue quality, not just revenue growth

Top-line growth gets attention, but revenue quality earns conviction. Investors want to know whether the company is growing from the right customers, through a repeatable motion, at margins that can survive scale.

A business can show impressive growth and still be difficult to underwrite. Revenue may be concentrated in a few accounts. New logos may require heavy discounts. Expansion may depend on the founder personally closing deals. Implementation costs may quietly erode gross margin. Churn may be hidden by new customer acquisition.

Quality revenue is revenue that can be explained, renewed, expanded, and forecasted.

| What investors examine | What they are really testing |

|---|---|

| Revenue growth by customer segment | Whether growth comes from the ideal customer profile or from opportunistic wins |

| Gross margin trends | Whether scale improves economics or adds delivery burden |

| Retention and expansion | Whether customers continue to value the product or service after the initial sale |

| Customer concentration | Whether the company is exposed to one or two accounts changing direction |

| Discounting patterns | Whether demand is strong enough to support pricing discipline |

| Pipeline conversion | Whether future revenue can be forecast with confidence |

This is where many companies misread investor interest. Growth equity firms are not impressed by a number in isolation. They want the story behind the number, then they want the data to support it.

2. A clear ideal customer profile and market expansion logic

Growth capital is often used to expand, but investors want to know precisely where expansion should happen and why.

A vague total addressable market rarely helps. Saying the market is worth billions does not prove the company can win a meaningful share of it. Investors want a sharper view: which customer segment buys fastest, stays longest, expands most, costs least to serve, and produces the strongest proof for the next segment?

That clarity matters because growth equity capital can easily be wasted on unfocused expansion. Hiring salespeople before the ideal customer profile is clear can increase burn without improving conversion. Entering a new geography without knowing which use case travels best can create expensive distraction. Launching new vertical campaigns without proof of sales velocity can make the company look busy while weakening the revenue engine.

The strongest companies can explain their beachhead market, their adjacent opportunities, and the sequence in which they plan to attack them. If you are preparing for that stage, the commercial foundations are similar to those covered in what every portfolio company needs before scaling: clear positioning, disciplined sales process, reliable data, and a realistic plan for capacity.

3. A repeatable go-to-market system

Founder-led selling is not a flaw. In many companies, it is how the first version of the commercial engine gets built. But by the time growth equity firms invest, they want to see that the company can move beyond founder dependency.

A repeatable go-to-market system does not mean every sale is identical. It means the company understands how demand is created, how opportunities progress, why customers buy, where deals stall, and which activities predict future revenue.

Strong signals include documented sales stages, stage exit criteria, conversion rates by source, marketing-to-sales handoffs, clean CRM discipline, defined sales roles, usable enablement materials, and a forecast methodology that does not depend on optimism.

Weak signals include a bloated pipeline, inconsistent definitions of qualified opportunities, unclear ownership between sales and marketing, high variance between reps, or a revenue forecast that changes dramatically from one week to the next.

This is one of the most important diligence areas because a company can show historical growth without having a scalable commercial machine. That hidden gap is the same issue discussed in the context of historical growth without a reliable commercial engine. Growth investors are trying to determine whether past performance reflects a system, a market tailwind, or a few exceptional individuals.

4. Leadership depth and operating cadence

Growth equity firms invest in management teams, not spreadsheets. The numbers matter, but the team must be capable of absorbing capital, making decisions quickly, and operating with greater transparency after the investment.

Investors look for a leadership team that understands its own constraints. A credible CEO does not need to have every answer. In fact, pretending there are no gaps often reduces trust. What matters is whether the team can identify the gaps, recruit around them, and operate with discipline.

Leadership depth becomes especially important when the investment plan depends on hiring, market expansion, or sales process transformation. If every major decision depends on one founder, scale becomes fragile. If the second layer of leadership is underdeveloped, growth may slow as complexity increases.

A strong operating cadence usually includes clear KPIs, regular performance reviews, accountability by function, and a management team that can distinguish between a temporary miss and a structural problem. Investors want to know that when capital is deployed, the company will learn quickly and adjust before small issues become expensive ones.

5. A use-of-funds plan tied to value creation

One of the fastest ways to weaken a growth equity conversation is to describe the use of funds too generically. Hiring more salespeople, increasing marketing spend, and entering new markets may all be valid, but only if the company can explain the assumptions behind them.

An investor-ready use-of-funds plan connects capital to measurable value creation. It shows what will be funded, why now is the right time, which milestones will prove progress, and what management will do if the assumptions are wrong.

| Weak use-of-funds statement | Investor-ready version |

|---|---|

| We will hire more salespeople | We will add quota capacity after validating conversion by segment and ramp assumptions |

| We will expand marketing | We will increase spend in channels with proven acquisition economics and track pipeline quality by source |

| We will enter the U.S. market | We will test a defined customer segment, build local proof, and expand only after conversion and retention signals are confirmed |

| We will invest in operations | We will remove delivery bottlenecks that currently limit gross margin and customer expansion |

Growth equity firms want to see that capital is not being used to compensate for uncertainty. They want it to accelerate a plan that has been pressure-tested.

6. Clean diligence materials and data integrity

A messy data room rarely kills a good company by itself, but it creates friction, slows the process, and gives investors reasons to reduce confidence.

Before investing, growth equity firms will review financial statements, revenue segmentation, customer contracts, sales pipeline, churn and retention data, pricing history, hiring plans, legal documents, and customer references. If the numbers in the deck do not match the numbers in the CRM or finance system, the issue becomes bigger than administration. It becomes a trust problem.

Clean data tells investors that management understands the business. It also allows them to move from basic verification to higher-value questions about strategy, growth levers, and risk mitigation.

What growth equity firms test in commercial due diligence

Commercial due diligence is where the investment story meets the market. Investors are trying to validate whether customers care enough, whether competitors can easily respond, whether pricing has room to improve, and whether the sales motion can scale.

They may speak with customers, former customers, prospects, industry experts, and competitors. They may analyze win-loss data, review sales calls, inspect the pipeline, and compare management's forecast with historical conversion patterns.

One underappreciated area is the quality of commercial proof. A strong brand story does not replace unit economics, but it can support buyer education, trust, and conversion when it is tied to the sales process. For companies where product complexity or credibility matters, assets such as demos, customer proof, and cinematic business promos can help communicate value, provided management can connect those assets to measurable funnel outcomes.

The key is not production polish for its own sake. It is evidence that the company understands how buyers make decisions and has built assets that help them move with confidence.

Red flags that can slow or kill the investment

Most growth equity firms expect imperfections. The issue is not whether a company has risk. The issue is whether the risk is visible, manageable, and already being addressed.

Common red flags include:

- Revenue growth driven by customers outside the stated ideal customer profile.

- High customer concentration with no credible diversification plan.

- Founder-dependent sales with limited evidence that other sellers can win.

- Churn explained away as bad-fit customers without clear segmentation data.

- A large pipeline with weak stage definitions or poor historical conversion.

- Heavy discounting that suggests limited pricing power.

- Hiring plans that assume productivity without evidence of ramp time or enablement.

- Inconsistent metrics across finance, sales, and board materials.

- A leadership team that cannot explain missed forecasts with precision.

The presence of one red flag does not automatically end a deal. A pattern of unexplained red flags does. Investors can underwrite risk, but they struggle to underwrite confusion.

How to prepare before approaching growth equity investors

The best preparation starts well before the fundraising process begins. Companies that wait until diligence to clean up metrics, clarify positioning, or inspect pipeline quality often find themselves reacting under pressure.

A better approach is to run an internal investment-readiness process 90 to 180 days before outreach. The goal is not to manufacture a perfect story. It is to identify the commercial evidence that already exists, fix the gaps that can be fixed, and be transparent about the issues that remain.

| Preparation move | Confidence it builds |

|---|---|

| Segment revenue by customer type, product line, geography, and acquisition source | Shows where growth is strongest and most repeatable |

| Audit CRM hygiene and pipeline stage definitions | Improves forecast credibility |

| Analyze retention, expansion, and churn by cohort | Proves whether customers continue to create value |

| Document sales process and handoffs | Reduces perceived dependency on individuals |

| Interview customers and lost prospects | Validates market need and competitive positioning |

| Build a milestone-based use-of-funds plan | Shows capital discipline and execution readiness |

| Identify leadership gaps honestly | Demonstrates maturity and coachability |

This preparation also improves the company's negotiating position. When management can answer investor questions with clean data and clear logic, the conversation shifts from proving basic credibility to discussing value creation.

What changes after investment

The pre-investment bar is high because the post-investment expectations are higher. Once growth equity capital is in the business, the company will usually face more rigorous reporting, tighter KPI management, and greater pressure to execute against the plan.

That can be a positive force if the company is ready. The right investor can bring strategic guidance, recruiting support, market perspective, acquisition experience, and board-level discipline. But capital does not remove the need for commercial infrastructure. It amplifies the need for it.

This is why companies should think about growth equity readiness as an operating project, not a fundraising project. The same evidence that wins investor confidence also helps the business scale more effectively after the deal closes.

Frequently Asked Questions

What is the difference between growth equity and venture capital? Venture capital often funds earlier-stage companies where product-market fit may still be developing. Growth equity typically backs companies with meaningful revenue traction and focuses on scaling a business that has already proven demand.

Do growth equity firms require profitability before they invest? Not always. Some will invest in companies that are not yet profitable if growth quality, margins, retention, and unit economics support the case for future profitability. The key is whether losses are strategic and controlled, not accidental.

What metrics matter most to growth equity firms? The most important metrics depend on the business model, but investors commonly examine revenue growth, gross margin, retention, expansion, customer concentration, sales efficiency, pipeline conversion, CAC discipline, and forecast accuracy.

How early should a company prepare for growth equity fundraising? Ideally, preparation should begin several months before outreach. This gives management time to clean data, validate the revenue story, improve pipeline discipline, and build a stronger use-of-funds plan.

What can kill a growth equity deal late in diligence? Late-stage issues often include inconsistent metrics, undisclosed churn, weak customer references, unreliable pipeline, unclear leadership ownership, legal or contract problems, or a use-of-funds plan that does not match the growth thesis.

Build the commercial evidence before the raise

Growth equity firms want more than ambition. They want a company that can show where growth comes from, why customers stay, how the sales engine works, and how new capital will create measurable value.

If you are a PE firm, VC, family office, or portfolio-company leadership team preparing for growth investment, Phil Pelucha Consulting helps diagnose revenue gaps, strengthen go-to-market systems, support market expansion, and install commercial infrastructure that improves growth and exit readiness.

The strongest time to fix the revenue engine is before diligence exposes the gaps. The second-best time is now.